Lightrun Answers was designed to reduce the constant googling that comes with debugging 3rd party libraries. It collects links to all the places you might be looking at while hunting down a tough bug.

And, if you’re still stuck at the end, we’re happy to hop on a call to see how we can help out.

[ENH] AutoETS to ignore multiplicative components when time series is not strictly positive

See original GitHub issueIs your feature request related to a problem? Please describe. If a time series is not strictly positive, ETS models (from statsmodels) with multiplicative components will raise the following error:

ValueError: endog must be strictly positive when usingmultiplicative error, trend or seasonal components.

Currently AutoETS will raise the same error because it tries all the available ETS models. Ideally AutoETS will skip the models that result in this error and will try all the other ones.

Describe the solution you’d like One solution would be to add a try/except in the _fit method. The other solution I can think of is to check whether the time series is strictly positive and if it’s not remove the multiplicative components from _iter.

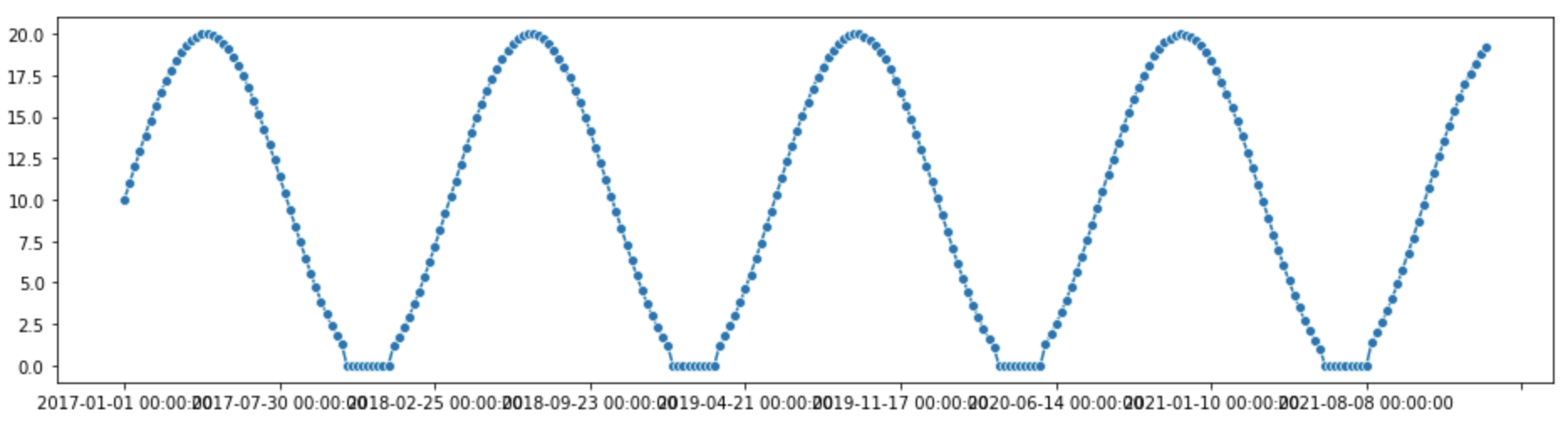

The following code reproduces the error:

import pandas as pd

import numpy as np

from sktime.forecasting.ets import AutoETS

from sktime.utils.plotting import plot_series

ts = pd.Series(

10*np.sin(np.array(range(0,264))/10)+10,

pd.date_range("2017-01-01", periods=264, freq="W")

)

ts[ts<1]=0

forecaster = AutoETS(auto=True, sp=52, n_jobs=-1, ignore_inf_ic=True)

plot_series(ts)

forecaster.fit(ts)

Issue Analytics

- State:

- Created 2 years ago

- Comments:9 (3 by maintainers)

Top Related StackOverflow Question

Top Related StackOverflow Question Troubleshoot Live Code

Troubleshoot Live Code Top Related Reddit Thread

Top Related Reddit Thread Top Related Hackernoon Post

Top Related Hackernoon Post Top Related Tweet

Top Related Tweet Top Related Dev.to Post

Top Related Dev.to Post Top Related Hashnode Post

Top Related Hashnode Post

@mloning, I’m sorry for the late reply. The fable version in R seems to check for this error as well so I think the second approach makes sense.

Thanks @HYang1996! So I suggest we implement that check in our version too and add a short note to the docstring.